It is estimated that 55 billion gallons of SAF will be required from the gasification of municipal waste by 2050.

Between 5-10 tonnes of municipal waste is required to produce 1 tonne of SAF. To avoid excessive transportation costs, it is imperative that waste to liquids plants are located close to the waste source. ASA, with its partners, will construct modular units with an output as low as 100 barrels/day to facilitate this. It is estimated that 45% of 2050 SAF demand will be met by waste to fuels and thousands of facilities will be required to meet this demand.

ASA’s engineering partner, Cross EPC (Pty) limited has designed and constructed an interface module that cleans and enhances the hydrogen content of the synthetic gas produced from waste gasification before it is fed to ASA’s reactive distillation column. This equipment is critical where synthetic gas is derived from gasification processes.

290 airlines have signed up to achieving Net Zero by 2050. These airlines will enter into long term contracts to secure SAF and this facilitates the financing of the waste to fuels projects.

Industrial offgas to SAF and petroleum products

Some of the world’s largest heavy industries (blast furnaces for iron and steel) produce a waste gas that has a significant carbon monoxide content and some hydrogen. Whilst some processes burn this waste gas for electricity generation, a significant proportion of the waste gas is flared with a significant impact on greenhouse gas emissions.

ASA’s process is able to convert this waste gas into synthetic crude that can be consumed either in the industrial process or further refined for end product usage.

Whilst there is a drive to utilise hydrogen in these processes or use next generation electric arc furnaces, there remains a significant number of relatively modern blast furnaces where ASA’s technology could be applied.

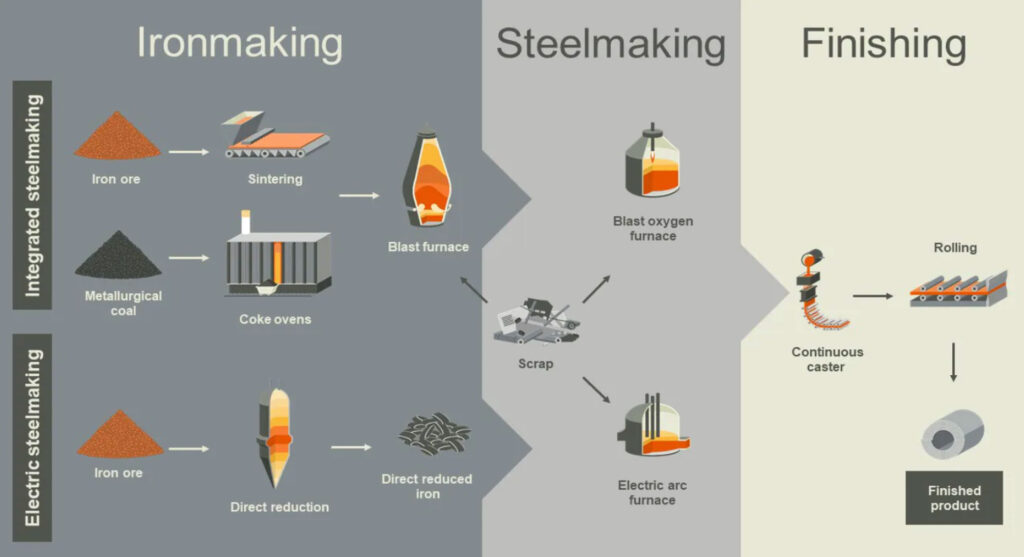

Figure 1: major steelmaking process routes

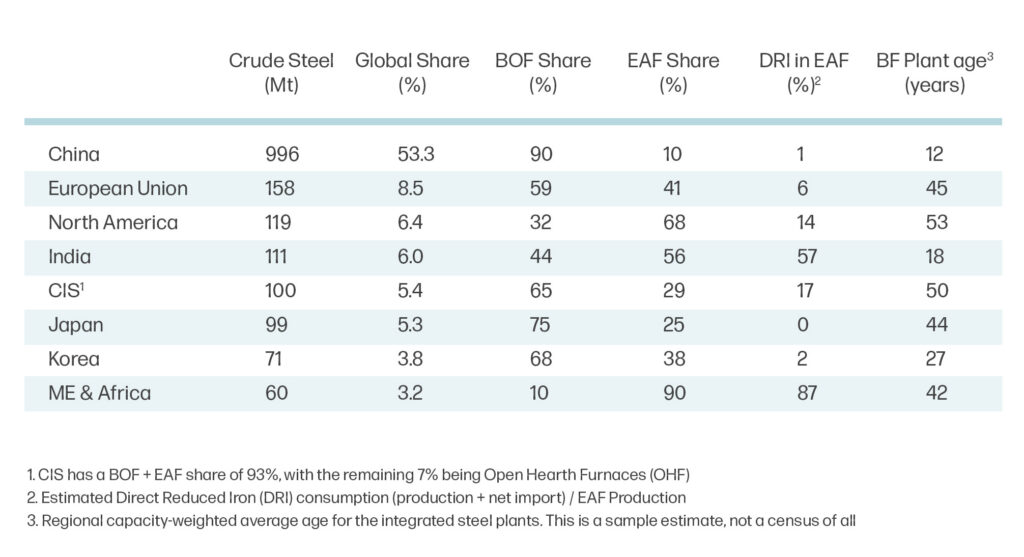

Table 1: snapshot of global steelmaking as of 2019 (Sources: worldsteel, BHP estimates)

This is a multi-billion-dollar market especially in China, Brazil and India where a significant proportion of these industries are located.

It is estimated by Global Energy Monitor that for environmental reasons, blast furnaces could become inoperable overtime leaving stranded assets of between US$345 and US$518 billion. ASA’s technology could significantly improve the environmental impact of these blast furnaces by utilising the waste gases.

Flared gas to petroleum products

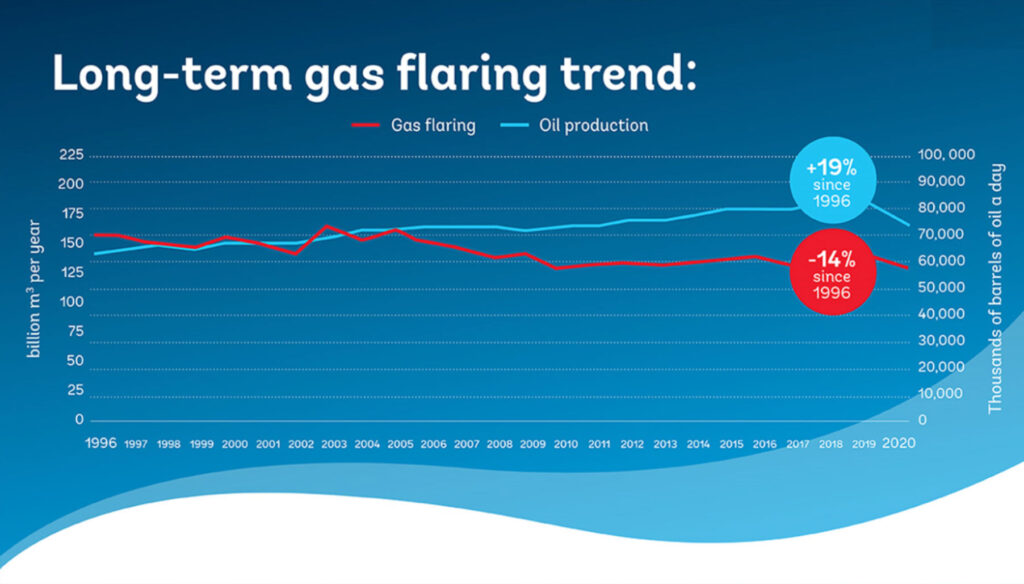

It is estimated that circa 143 Bcm or 5 Tcf of gas was flared in 2021. This is the equivalent of 841 million barrels of oil. This generates circa 400 million tonnes of carbon dioxide emissions including un-combusted methane and black carbon.

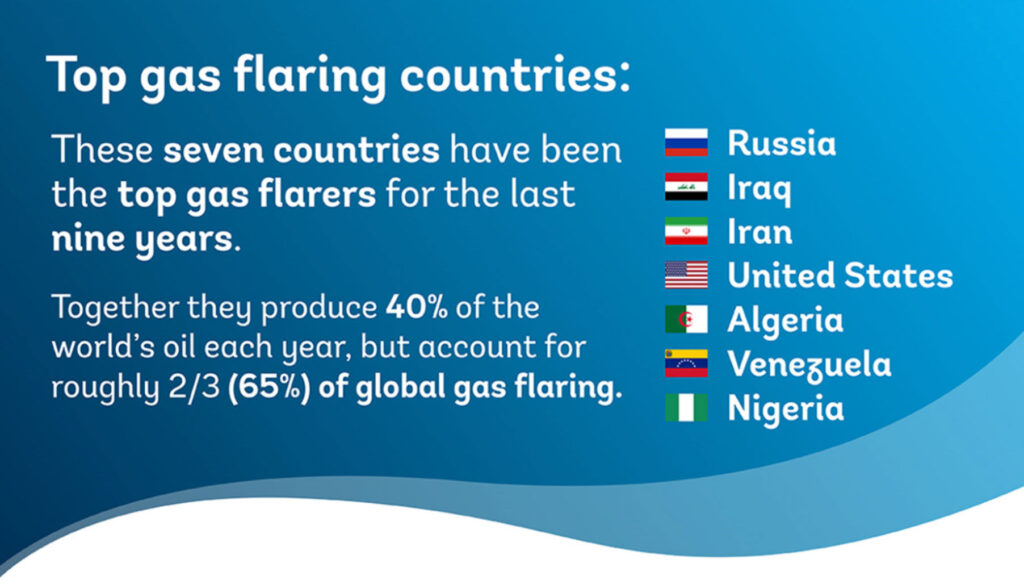

Where it is flared in adequate quantities (>5 MMscf/d), ASA could convert this gas into synthetic crude so that it could be blended and transported to markets utilising existing oil infrastructure. There are a small number of large flaring sites which contribute the most to global flaring. In 2020, 12 percent of flare sites contributed to 75 percent of total flaring volume globally.

Given the compact size of ASA’s natural gas to liquids facility, it is expected that ASA’s technology will ultimately be incorporated in a Floating Production, Storage and Offtake vessels for the processing of associated gas offshore. This could be particularly valuable for those offshore developments that are a significant distance from gas markets.

Air to fuel

Air to fuel is expected to account for 50% of SAF demand by 2050. The electrolysis of water to produce hydrogen using wind and solar can be combined from captured carbon dioxide to deliver a clean synthetic gas. ASA’s technology is then ideally suited to convert this into SAF.

Green hydrogen could also be combined with industrially produced carbon monoxide.

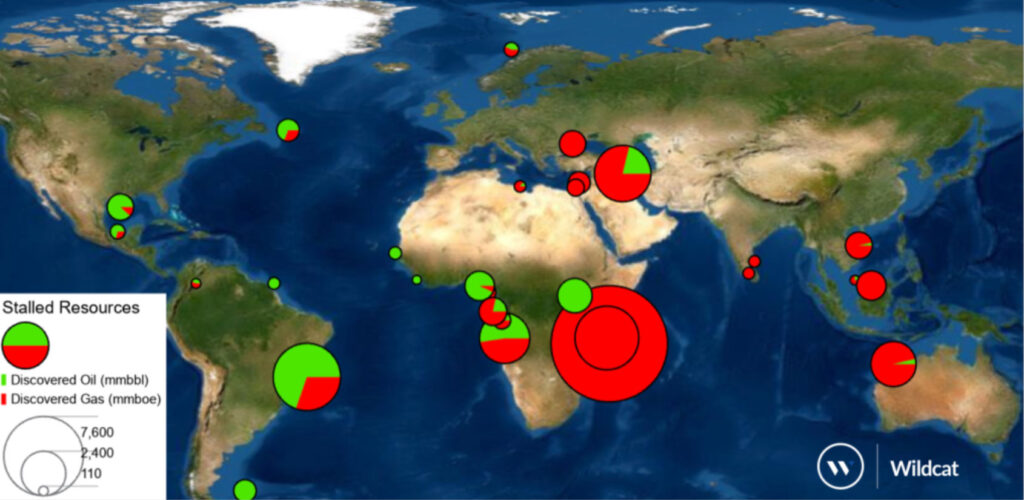

Stranded gas assets

There are numerous onshore and offshore stranded gas fields worldwide that have not been developed. This is frequently because local gas demand is too small to justify an economic development, or the resources are too small to justify an LNG project.

ASA’s GTL’s process will open a number of these opportunities as the gas resources will be converted into a fungible product that can be consumed domestically or exported. It significantly enhances the bankability of any gas project and may facilitate the development of a domestic gas industry concurrently.

This is particularly the case for several countries in sub-Saharan Africa that are long gas and short petroleum products. The conversion of gas to liquids would have a significant positive impact on their economies as gas displaces oil or coal in electricity generation and oil imports are reduced or eliminated.

Location map of stalled resources - Credit: Westwood Energy